If the financial needs of your company are irregular, while its revenue is steady, Revolving Credit is the ideal financing facility for your company. Revolving Credit offers your business a line of credit that can be used only when needed, as needed, and more importantly as many times as needs arise, as long as you stay within the maximum credit limit. Moreover, Revolving Credit provides a great deal of flexibility in that no fixed monthly payment is stipulated. Your balance can be revolved, i.e. carried from month to month.

Like other types of Corporate Financing, some profit has to be paid to the financing bank under Revolving Credit, in addition to associated service charges and fees. The following equation summarizes the essential components of Revolving Credit:

Total Financing Amount = Financing Amount + Bank’s Profit + Associated Fees

In this section, we will discuss the second component of the previous equation.

The following table summarizes the important differences between the two types of financing.

Revolving Credit |

Non-Revolving Credit |

|---|---|

Can be used repeatedly within the terms of the facility | Can be used once; A fresh agreement is needed for additional funds |

Involves higher risk, and thus typically has lower credit limit and higher profit rate | Relatively lower risk |

Requires cautious financial management to avoid debt crisis due to excessive use of revolving | Payment schedule is fully predictable once the Financing Amount is determined |

This is the maximum amount of money you can receive at any point of time. As previously mentioned, you do not need to utilize this amount at once, or to ever utilize it all. You can make several utilizations, each with the desired amount and at the suitable time. Additionally, you can utilize the available credit repeatedly within the Financing Term. No agreed upon schedule with MBSB Bank is required. Just make sure that every utilization is preceded with a 7-day written notice.

In Tawarruq terminology, the Financing Amount corresponds to the Purchase Price, while the Financing Amount plus the maximum profit correspond to the selling price.

This is the amount of money made by the financing bank in return of offering and administering the facility for you. Profit is proportional to the amount of utilized funds and to the period of time you take to pay them. The more these funds are and the longer it takes to be settled, the more the profit will be. Profit is linked to the amount of utilized funds through the Effective Profit Rate.

MBSB Bank calculates the Profit as a percentage of the actually utilized funds on a daily basis. This percentage is the Effective Profit Rate (EPR). The profit is usually paid on a monthly or quarterly basis. Please note that as you settle some or all of the outstanding balance, the profit decreases or cease to roll in respectively.

It is important to realize that EPR does not necessarily remain unchanged during the entire financing term. This is because MBSB Bank applies a variable profit rate scheme, rather than a fixed one. Accordingly, the Profit rate you have to pay may change during the financing term, see Financial Risks.

EPR consists of two components: Base Rate (BR) and profit margin. BR is the minimum EPR that MBSB Bank may use in Revolving Credit. Remember that BR may change during your financing term. Profit margin is the additional profit component added to BR to make the EPR. Apparently, you are more concerned with EPR than BR.

As a measure of customer protection, EPR cannot simply increase without a limit. The maximum value that EPR may ever rise to is called the Ceiling Profit Rate (CPR). CPR, thus, represents the worst case of your Revolving Credit.

Revolving Credit does not cover the entire financial needs of your project(s). You have to pay a portion of these needs outside the financing facility. This Down Payment portion is usually 20-30% of the total needed funds. In such case, the Financing Margin is 70-80%.

The Maturity Date refers to the date by which you must pay the Financing Amount plus all incurred amounts of profit in full. On that date, profit payments will cease to roll in. Unsettled payments after that date will be considered default payments.

If you need more time to settle an outstanding balance, you may rollover, subject to the bank’s approval, this balance to a new later maturity date. Please note that MBSB Bank may apply a different EPR figure upon rollover.

Financing Term, or Tenure, is the period between the first utilization of the facility and the Maturity date. Kindly note that the first utilization has to be done within the availability period of the facility, or the facility may be cancelled.

What does a customer gain or lose from prolonging or shortening the tenure? Apparently, a longer tenure gives you a longer time to re-utilize the available credit if you need to do so. As you hit the maturity date, you have to discharge all your financial obligations to avoid the consequences of being at default. Once again, a prudent financial management is imperative to avoid the temptation of unnecessary revolving of your balance, which could put you in a serious debt mess.

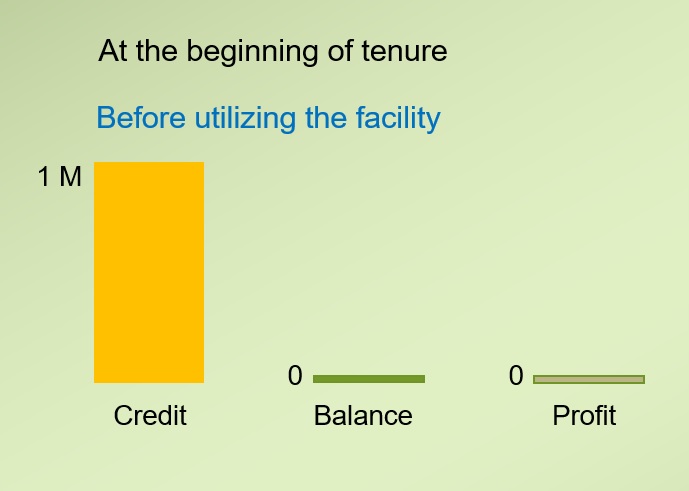

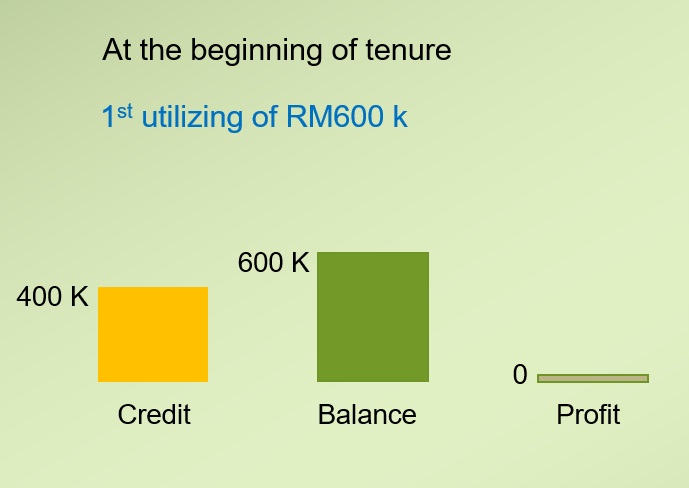

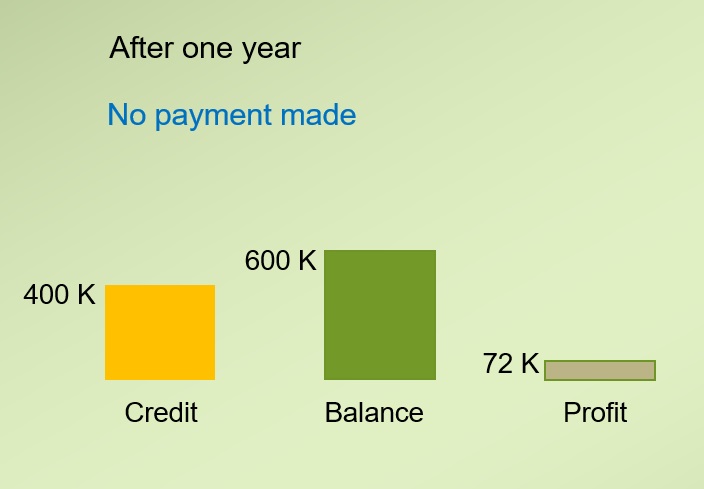

To understand the operational mechanism of Revolving Credit, you have to be familiar with two terms: available credit and outstanding balance, or simply balance. Before utilizing the facility, the available credit is equal to the Financing Amount (credit limit) and the balance is zero. After utilizing the full Financing Amount, the available credit is zero and the balance is equal to the Financing Amount. Available credit and balance add up to a single number, which is the Financing Amount. At any point of time, no utilization can exceed the available credit.

Once you utilize the facility, you have to start making the profit payments associated with the actually received funds on a monthly or quarterly basis, as agreed. The due profit is directly proportional, via EPR, to the unsettled Financing Amount.

Your payments naturally go to two components: the Financing Amount and the due profit by then. As previously discussed, profit changes depending on the current outstanding balance. How much of each payment goes to each one? To answer this question, the following simple rule is introduced:

The underlying payment fulfills the due profit first, and the rest goes towards the Financing Amount.

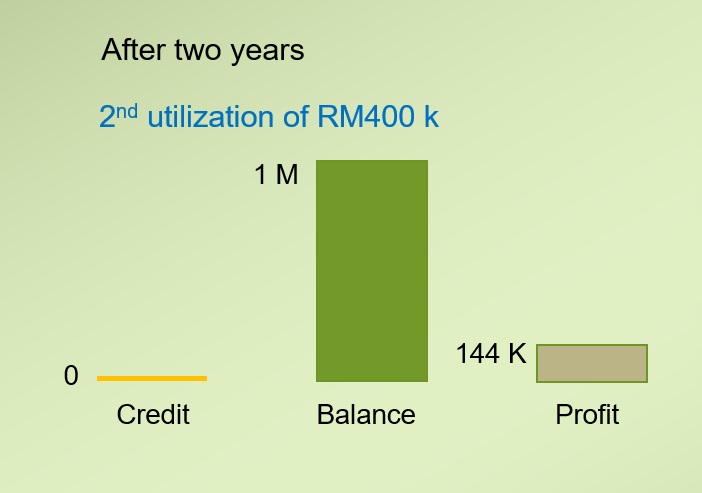

Suppose that Great Products Enterprise has been offered a Revolving Credit facility from MBSB Bank. The Financing Amount of this facility is RM1 M, EPR is 12%, and the tenure is 3 years. In this case, it is assumed that Great Products will settle its indebtedness on the Maturity Date. The following snapshots show how the available credit, balance, and profit change during the tenure.

On the Maturity Date, a total of RM1,264,000 is due.

You can save some money by using one of the following options:

As you know, Revolving Credit scheme follows a variable profit rate. If EPR rises, you will incur an additional profit for the remaining of your financing term. The following table lists the total profit for EPR of 12%, 13%, and 14% for a utilization of RM1 M over 3 years. Calculations are made based on the assumption that EPR increased at the very beginning of the financing term.

EPR |

12% |

EPR goes up by 1% |

EPR goes up by 2% |

|---|---|---|---|

Total Profit | 360,000 | 390,000 | 420,000 |

Please note that you may run into a higher EPR if you rollover an outstanding balance to a later Maturity Date.