When you buy a property through a bank financing, you will be paying the property price to the developer/seller, some profit to the bank that is financing you, and associated costs and fees. The following equation summarizes the essential components of home financing:

Total Financing Amount = Property Price + Bank’s Profit + Associated Fees

In this section, we will discuss the second component of the previous equation. The third component will be discussed in the next section.

This is the amount of money made by the financing bank in return of offering and administering the home financing for you. In the context of the Tawarruq process, Profit is the difference between the selling price you pay to MBSB Bank by way of instalments and the cost price, see My Journey with MBSB Bank.

MBSB Bank calculates the Profit as a percentage of the current balance of your Financing Amount on a monthly basis. It is important to note that since the balance of the Financing Amount decreases every month, as you are making your monthly payments, the profit you pay every month also decreases. The ratio of the monthly profit to the current balance of the Financing Amount (after dividing it by 100 to give the value in percent) is the Effective Profit Rate (EPR). EPR does not necessarily remain unchanged during the entire financing term. This is because MBSB Bank applies a variable profit rate scheme, rather than a fixed one. This means the amount of Profit you have to pay may change during the financing term, see Risks.

As a measure of customer protection, EPR cannot simply increase without a limit. The maximum value that EPR may ever rise to is called the Ceiling Profit Rate (CPR). CPR, thus, represents the worst case of your home financing.

EPR consists of two components: Base Rate (BR) and profit margin. BR is the minimum EPR that MBSB Bank may use for home financing. Please check www.mbsbbank.com for the current BR. Remember that this figure may change, even if your financing term begins with. Profit margin is the additional profit component added to BR to make the EPR. Apparently, you are more concerned with EPR than BR.

In addition to the property value, your property financing from MBSB Bank also covers the single payment of MRTT. The legal fee, up to RM 6000 is covered for the My First Home Package (the rest is borne by you). In common business accounting terminology, this amount is referred to as the Financing Amount. In your Letter of Offer from MBSB Bank, it is called the Purchase Price, following the Tawarruq terminology.

Most banks require you to pay a portion of the property price out of your own personal money, outside the financing agreement. This Down Payment portion is usually 10-20% of the property price. If the Down Payment is 10%, the finance margin is 90%. If the Down payment is 20%, the finance margin is 80%. Only for property financing schemes targeting lower income groups, the finance margin can go up to 100%. Down Payment required for commercial properties is usually higher than that for residential ones.

For properties under construction, a Grace Period (GP) is offered to borrowers. During GP, the concerned customer is released from paying the monthly instalments. MBSB Bank’s disbursements of the property value to the developer are made during GP, too. GP can extend up to 4 years.

Grace Period Profit (GPP) depends on actual disbursed amount(s) received by your developer/seller. Your annual GPP is calculated as follows:

Annual GPP = Amount disbursed x EPR

Annual GPP will be paid in arrays of 12 monthly payments as follows:

Monthly GPP = Amount disbursed x EPR x (no. of days/365)

Consider a Financing Amount of RM 300,000.00, with EPR of 4.55%. Assume that RM 100,000.00 was disbursed in the beginning of the financing term, RM 100,000.00 was disbursed after one year, and RM 100,000.00 was disbursed after two years. To simplify the GPP calculations, let us assume that all months are 30 days (Actual GPP payments will slightly differ). GPP payments will be as follows:

First year monthly GPP payment = 100,000 x 4.55% x (30/365) = RM 373.97

Second year monthly GPP payment = 200,000 x 4.55% x (30/365) = RM 747.94

Your GP expires by making the final disbursement after two years. Your monthly instalments will start as of the third year.

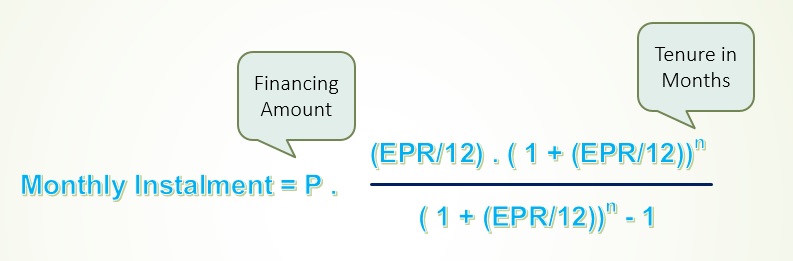

As previously discussed, Profit changes every month depending on the balance of the Financing Amount. Nonetheless, you probably know that your monthly instalments remain fixed over the financing term, unless EPR changes. This is the outcome of Amortization. Amortization is the process of spreading out a financing amount into a series of fixed payments over the financing term. If you are curious to see the amortization formula, hover over the image below:

The Amortization formula calculates monthly instalments based on the Financing Amount, EPR, and the financing term. These instalments pay two things: the Financing Amount and the Profit. How much of the monthly instalment goes to each one? To answer this question, the following simple rule is introduced:

A monthly payment fulfills the monthly profit first, and the rest goes towards the Financing Amount.

Now, let us take a numerical example. For a Financing Amount of RM 100,000, EPR of 4.55%, and a tenure of 30 years, the 12 monthly instalments of the first year will be divided as follows:

Month |

Starting Balance |

Monthly Instalment |

Monthly Profit |

Monthly Principal |

Ending Balance |

Total Profit |

|---|---|---|---|---|---|---|

1 | 100,000.00 | 509.66 | 379.17 | 130.49 | 99,869.51 | 379.17 |

2 | 99,869.51 | 509.66 | 378.67 | 130.99 | 99,738.52 | 757.84 |

3 | 99,738.52 | 509.66 | 378.18 | 131.49 | 99,607.03 | 1,136.01 |

4 | 99,607.03 | 509.66 | 377.68 | 131.98 | 99,475.05 | 1,513.69 |

5 | 99,475.05 | 509.66 | 377.18 | 132.48 | 99,342.56 | 1,890.87 |

6 | 99,342.56 | 509.66 | 376.67 | 132.99 | 99,209.58 | 2,267.54 |

7 | 99,209.58 | 509.66 | 376.17 | 133.49 | 99,076.09 | 2,643.71 |

8 | 99,076.09 | 509.66 | 375.66 | 134.00 | 98,942.09 | 3,019.37 |

9 | 98,942.09 | 509.66 | 375.16 | 134.51 | 98,807.58 | 3,394.53 |

10 | 98,807.58 | 509.66 | 374.65 | 135.02 | 98,672.57 | 3,769.17 |

11 | 98,672.57 | 509.66 | 374.13 | 135.53 | 98,537.04 | 4,143.31 |

12 | 98,537.04 | 509.66 | 373.62 | 136.04 | 98,401.00 | 4,516.93 |

As you know the monthly instalment is calculated by the amortization formula. Assume that you want to know how your 8th payment contributed to the Financing Amount and the Profit. The starting balance of the Financing Amount is RM 99,076.09. Then,

The monthly profit of the 8th month = 99,076.09 x (4.55/12) = RM 375.66, and

The Financing Amount payment component = 509.66 – 375.66 = RM 134.00

This Financing Amount payment component reduces the ending balance to RM 98,942.09, while the monthly profit component increases the total profit to RM 3,019.37. By the end of your financing term, the balance of the Financing Amount will be zero, and the 360 (30 year tenure) monthly profit payments will add up to make the total Profit.

Financing Term, or Tenure, is the period for paying the Selling Price, i.e. Financing Amount plus Profit. What does a customer gain/lose from prolonging/shortening the home financing tenure? Apparently, a longer tenure gives you a lower monthly instalment that fits your monthly budget. On the other hand, a longer tenure increases the amount of Profit, and subsequently the overall financing amount. Conversely, a shorter tenure saves you the extra amount of Profit associated with the longer tenure, but increases your monthly instalment. If your income can support a higher monthly instalment, most financial analysts think that you should opt for a shorter tenure.

Homebuyers searching for dream homes may focus on the big financial elements, like property value and the financing amount, while overlooking other significant costs associated with the sale procedure, as well as various legal fees. Closing costs refer to all costs incurred after signing the sale agreement until you actually own the house and become eligible to move into it. Closing costs can be anywhere from 3 to 6 percent of the total Financing Amount. Unless considered and properly factored in, closing costs could be a heavy burden on your budget.

Closing costs fall into 3 categories: costs associated with getting the financing facility, taxes paid to the government, and third-party fees. The following summarizes the most significant closing costs. Please note that other costs might still appear.

I. Costs for getting the financing facility

Processing fee: This is the charge for processing your application and producing your credit report. MBSB Bank waives the processing fee for most home financing products.

Valuation fee: The valuation process compares the value of the property to similar properties in the same neighborhood to ensure that the property is worth what the seller is asking for. It is done by professional evaluators who usually charge about 0.2% of the property value. MBSB Bank has its own list of such evaluators.

Legal fees paid to MBSB Bank’s solicitors for preparing financing documents, registering the charge at the Land Office, and doing necessary legal checks, such as land search and bankruptcy search of the developer. Please note that your developer talks about different legal fees paid to the attorney who is helping you with the SPA and transferring the ownership of the property to you.

Takaful coverage: Islamic banks require home buyers to buy Mortgage Reducing Term Takaful (MRTT), which provides financial protection for settling the outstanding Financing Amount in the event of death or permanent disability of the applicant(s). MRTT is usually 3-5% of the Financing Amount. MBSB Bank includes the basic contribution of the MRTT in the Financing Amount. Nonetheless, it is one of the financial obligations that you will have to fulfill. For more info, see MRTT.

II. Governmental taxes

Stamp duty: This is the tax placed on your property documents during the sale or transfer of the property. The sale or transfer of properties in Malaysia, which are chargeable with stamp duty, must be stamped within 30 days from the date of the execution. Stamp duty is calculated on a tiered-basis as a percentage of the purchase price. You will also need to pay stamp duty on your financing agreement based on a flat rate of 0.5% of 90% of the Financing Amount. You should check for the latest stamp duty rates, as well as potential waivers of it.

As you may have noticed stamp duty is independent of the home financing, and it is an unavoidable cost for buying a property.

III. Third-party fees

Attorney fee: Your attorney will offer you the legal assistance needed for concluding the closing process; He will prepare all documents and contracts required for transferring the property to you. Attorney fees in Malaysia vary from 0.5% to 1% of the property value. Please note that some developers absorb the legal fee for signing the Sale and Purchase Agreement (SPA), and it is definitely an item of negotiation with your developer/seller.

Title search fee: The purpose of this search is to ensure that the person claiming to be the owner of the property is indeed the legal owner. Public records that could affect ownership rights are examined to ensure that the title transfer process is not going to face a legal obstacle.

Property agent fee: If you employed a property agent to secure the property for you, his/her fee is usually about 3% of the property value.

Renovation costs: Obviously, if some renovation work is needed before you can move into your new house, such costs have to be considered too.

Apart from the closing costs, you can save some of the financing amount by using one of the following options:

30-year tenure |

15-year tenure | |

|---|---|---|

Monthly Instalment | 509.66 | 767.55 |

Total Profit | 83,477.79 | 38,159.60 |

No Extra Monthly Payment |

RM 100 Extra Monthly Payment |

RM 200 Extra Monthly Payment | |

|---|---|---|---|

Effective Tenure in Months | 360 | 257 | 202 |

Total Profit | 83,477.79 | 56,692.80 | 43,300.95 |

Less Profit | 0 | 26,784.99 | 40,176.84 |

EPR |

4.55% |

EPR goes up by 1% |

EPR goes up by 2% |

|---|---|---|---|

Monthly Instalment | 509.66 | 570.93 | 635.36 |

Total Profit | 83,477.79 | 105,534.81 | 128,729.55 |

As you know, your total financing amount equals the total profit plus the Financing Amount.

TIP: The above numbers can be adapted to your Financing Amount by simply multiplying them by Financing Amount/100,000. If your Financing Amount is RM 200,000, multiply them by 2.