❔

Definition: |

❔

Integrals:

|

❔

Conditions: |

❔

Supplementary contracts:

|

❔

Types:

|

❔

Profit:

|

❔

Products:

|

Deposit Accounts |

Consumer Finance |

Corporate Finance |

|

|---|---|---|---|

Purpose |

Provide cash growing instruments for individuals and corporates in a Shariah compliant environment. |

Provide funds needed by individuals for their personal and home-purchase needs. |

Provide funds for corporates for acquiring fixed assets, financing an investment, financing the business working capital, or bridging the gap in the business' liquidity needs. |

Types |

• Current Account-i |

• Personal Financing-i |

• Term Financing-i |

Shariah Mechanism |

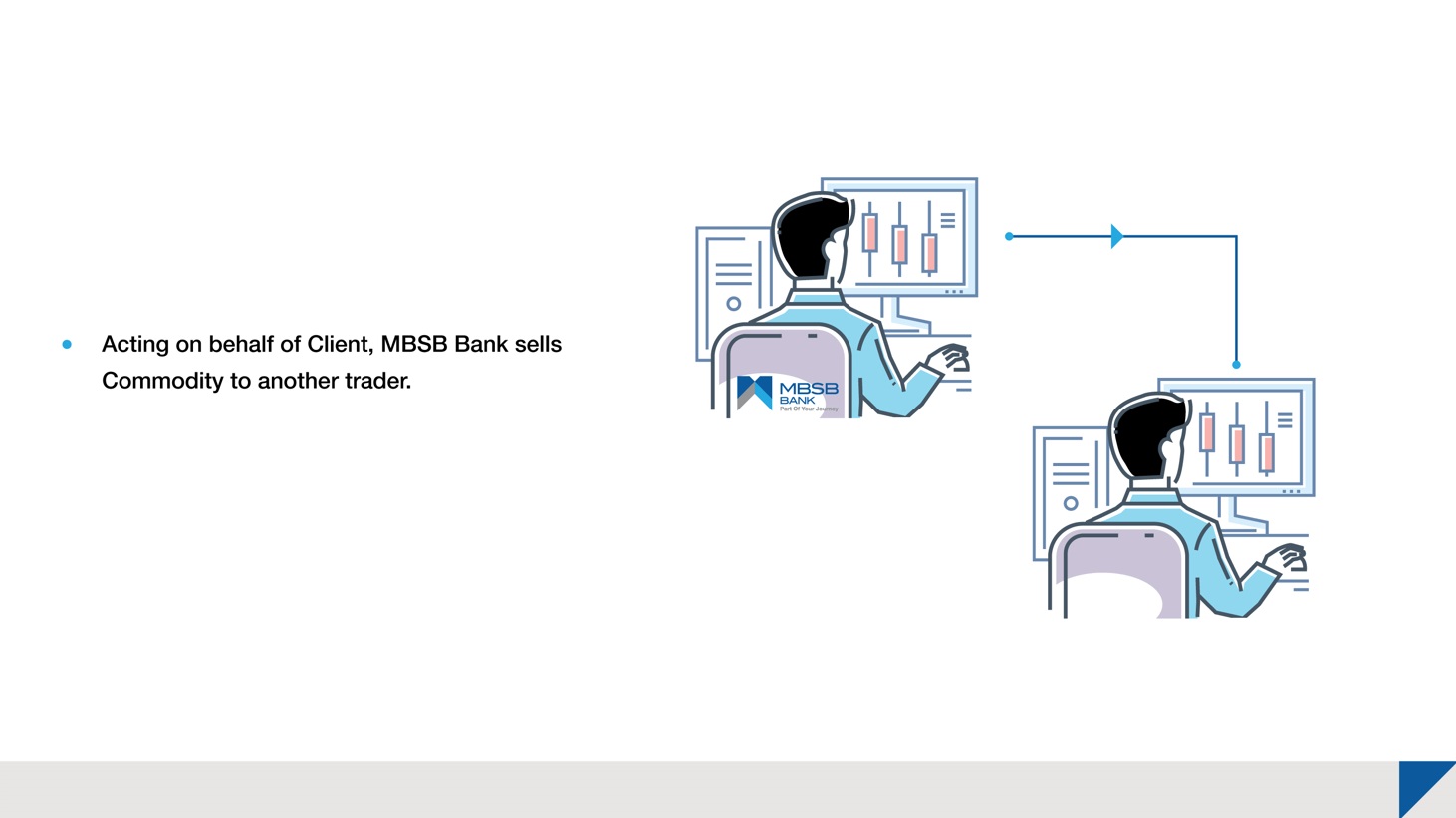

Reverse Tawarruq |

Tawarruq |

Tawarruq |

Learn More |

|

|

|