When you get a Personal Financing facility through a bank, you will be paying some profit to the bank that is financing you, in addition to associated costs and fees. The following equation summarizes the essential components of Personal Financing:

Total Financing Amount = Applied Financing Amount + Bank’s Profit + Associated Charges and Fees

In this section, we will discuss the bank’s profit. Associated charges and fees consist of Takaful coverage (optional), Late Payment Compensation, if any, and Wakalah fee.

This is the amount of money made by the financing bank in return of offering and administering the Personal Financing facility for you. In the context of the Tawarruq process, Profit is the difference between the selling price you pay to MBSB Bank by way of instalments and the cost price, see My Journey with MBSB Bank.

MBSB Bank calculates the Profit as a percentage of the current balance of your Financing Amount on a monthly basis. It is important to note that since the balance of the Financing Amount decreases every month, as you are making your monthly payments, the profit you pay every month also decreases. The ratio of the monthly profit to the current balance of the Financing Amount (after dividing it by 100 to give the value in percent) is the Effective Profit Rate (EPR). However, EPR does not necessarily remain unchanged during the entire financing term. This is because MBSB Bank applies a variable profit rate scheme, rather than a fixed one. This means the amount of Profit you have to pay may change during the financing term, see Risks.

As a measure of customer protection, EPR cannot simply increase without a limit. The maximum value that EPR may ever rise to is called the Ceiling Profit Rate (CPR). CPR, thus, represents the worst case of your Personal Financing.

EPR consists of two components: Base Rate (BR) and profit margin. BR is the minimum EPR that MBSB Bank may use with Personal Financing. Remember that BR may change, even if your financing term begins with. Profit margin is the additional profit component added to BR to make the EPR. Apparently, you are more concerned with EPR than BR.

This is the amount of money you apply to get, e.g. RM100,000. However, when MBSB Bank disburses this money into your account, fees and charges mentioned above will be deducted from it. Following the Tawarruq terminology, the Financing Amount is equivalent to the Purchase Price.

One or two (depending on your category) of your monthly payments will be deducted from your Financing Amount as a security deposit. This deposit will count as the last payment(s) of your financing tenure.

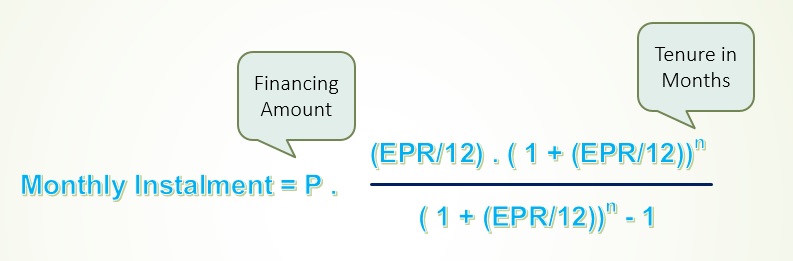

As previously discussed, Profit changes every month depending on the balance of the Financing Amount. Nonetheless, your monthly instalments remain fixed over the financing term, unless EPR changes. This is the outcome of Amortization. Amortization is the process of spreading out a financing amount into a series of fixed payments over the financing term. If you are curious to see the amortization formula, hover over the image below:

The Amortization formula calculates monthly instalments based on the Financing Amount, EPR, and the financing term. These instalments pay two things: the Financing Amount and the Profit. How much of the monthly instalment goes to each one? To answer this question, the following simple rule is introduced:

"A monthly payment fulfills the monthly profit first, and the rest goes towards the Financing Amount."

Now, let us take a numerical example. For a Financing Amount of RM100,000, EPR of 5.55%, and a tenure of 5 years, the 6 monthly instalments of the first year will be divided as follows:

Month |

Starting Balance |

Monthly Instalment |

Monthly Profit |

Monthly Principal |

Ending Balance |

Total Profit |

|---|---|---|---|---|---|---|

1 | 100,000.00 | 1,912.42 | 462.50 | 1,449.92 | 98,550.08 | 462.50 |

2 | 98,550.58 | 1,912.42 | 455.79 | 1,456.63 | 97,093.44 | 918.29 |

3 | 97,093.44 | 1,912.42 | 449.06 | 1,463.37 | 95,630.08 | 1,367.35 |

4 | 95,630.08 | 1,912.42 | 442.29 | 1,470.14 | 94,159.94 | 1,809.64 |

5 | 94,159.94 | 1,912.42 | 435.49 | 1,476.94 | 92,683.01 | 2,245.13 |

6 | 92,683.01 | 1,912.42 | 428.66 | 1,483.77 | 91,199.24 | 2,673.79 |

As you know the monthly instalment is calculated by the amortization formula. Assume that you want to know how your 4th payment contributed to the Financing Amount and the Profit. The starting balance of the Financing amount is RM95,630.08. Then,

The monthly profit of the 4th month = 95,630.08 x (5.55/12) = RM442.29, and

The financing payment component = 1,912.42 – 442.29 = RM1,470.14

This component reduces the ending balance to RM 94,159.94, while the monthly profit component increases the total profit to RM1,809.64. By the end of your financing term, the balance of the Financing Amount will be zero, and the 60 (5 year tenure) monthly profit payments will add up to make the total Profit.

Financing Term, or Tenure, is the period for paying the Selling Price, i.e. Financing Amount plus Profit. What does a customer gain/lose from prolonging/shortening the home financing tenure? Apparently, a longer tenure gives you a lower monthly instalment that fits your monthly budget. On the other hand, a longer tenure increases the amount of Profit, and subsequently the overall financing amount. Conversely, a shorter tenure saves you the extra amount of Profit associated with the longer tenure, but increases your monthly instalment. If your income can support a higher monthly instalment, most financial analysts think that you should opt for a shorter tenure.

You can save some of the Financing Amount by using one of the following options:

10-year tenure |

5-year tenure | |

|---|---|---|

Monthly Instalment | 1,087.74 | 1,912.42 |

Total Profit | 30,529.04 | 14,745.50 |

No Extra Monthly Payment |

RM100 Extra Monthly Payment |

RM200 Extra Monthly Payment | |

|---|---|---|---|

Effective Tenure in Months | 60 | 57 | 54 |

Total Profit | 14,745.50 | 13,887.99 | 13,125.67 |

Less Profit | 0 | 857.51 | 1,619.83 |

What if you fail to meet your financial obligations?

As summarized in the Product Description Sheet of personal financing, Par. 9, failing to meet your financial obligations, without agreeing with the bank on alternative payment arrangements, could result in the following consequences:

The bank has the right to charge you a compensation fee of 1% per annum on overdue payment(s). This fee cannot be further compounded in proportion to the overdue amount or in proportion to the elapsed time after missing the payment.

For example, if you miss a payment of RM10,000 for 2 years, the compensation fee will be RM100 for the first year, and RM100 for the second year. Since the compensation fee is charged on a monthly basis, you will be charged RM8.33 every month.

The Bank has the right to set-off any credit balance in your account maintained with the Bank against any outstanding balance in your financing facility account. The bank is going to issue a 7-day notice of the intended set-off. Of course, you should rectify the situation as soon as you receive this notice.

The Bank reserves the right to take legal action, which will have an effect on your credit rating.

As you know, your Personal Financing scheme follows a variable profit rate. If EPR rises, you will incur an additional profit for the remaining of your financing term. The following table lists the total profit for EPR of 5.55%, 6.55%, and 7.55% for a financing of RM100,000.00 over 5 years. Respective Monthly instalments are listed too. Please note that it is assumed that EPR increased at the very beginning of the financing term.

EPR |

5.55% |

EPR goes up by 1% |

EPR goes up by 2% |

|---|---|---|---|

Monthly Instalment | 1,912.42 | 1,958.96 | 2,006.16 |

Total Profit | 14,745.50 | 17,537.46 | 20,370.30 |

As you know, your total financing amount equals the total profit plus the Financing Amount.

TIP: The above numbers can be adapted to your financing case by simply multiplying them by Financing Amount/100,000. If your Financing Amount is RM200,000, multiply them by 2.